User guide¶

Contents

Models¶

The models that are currently implemented in fyne are the Black-Scholes,

Heston and Wishart models. In order to make notation clear, especially with the

naming of the parameters, we state below the discounted underlying price

dynamics of the models under the risk-neutral measure.

- Black-Scholes

- Heston

- Wishart

Pricing¶

Each model has its own pricing formula. The available pricing functions are:

These functions return the price of the option in monetary units. If implied

volatility is needed, it can be evaluated with

fyne.blackscholes.implied_vol().

Example¶

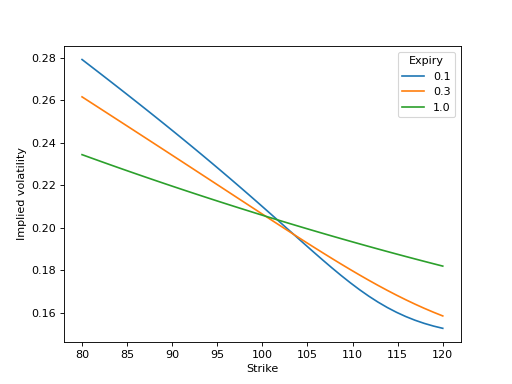

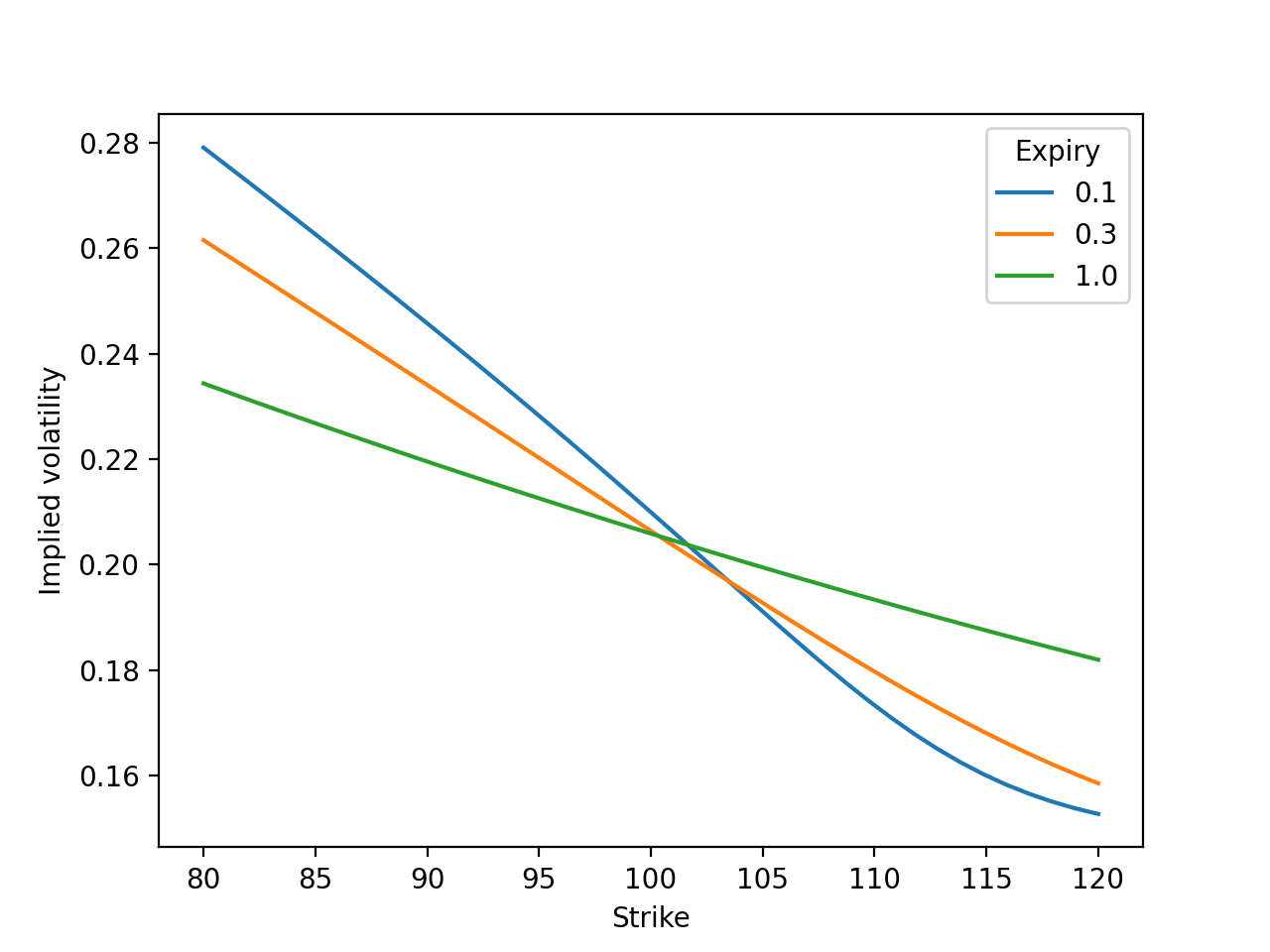

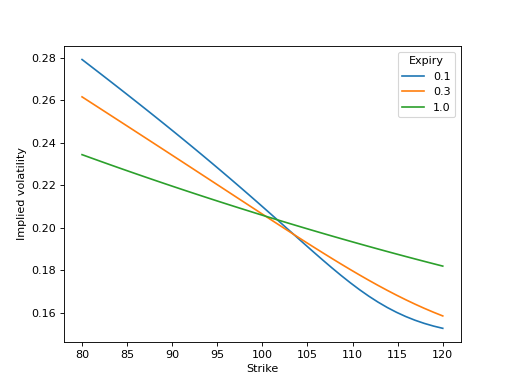

In this example, we compute the implied volatility smile according to the Heston model.

import numpy as np

import pandas as pd

from fyne import blackscholes, heston

underlying_price = 100.

vol, kappa, theta, nu, rho = 0.0457, 5.07, 0.0457, 0.48, -0.767

strikes = pd.Index(np.linspace(80., 120., 40), name='Strike')

expiries = pd.Index([0.1, 0.3, 1.0], name='Expiry')

option_prices = heston.formula(underlying_price, strikes[:, None], expiries,

vol, kappa, theta, nu, rho)

implied_vols = pd.DataFrame(

blackscholes.implied_vol(underlying_price, strikes[:, None], expiries,

option_prices),

strikes, expiries)

implied_vols.plot().set_ylabel('Implied volatility')

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

Greeks¶

Greeks are usually associated to the derivatives of the Black-Scholes formula.

However, Greeks can be computed according to other models as well. The following

are the available Greeks in fyne:

Calibration¶

In fyne we distinguish two types of calibration:

- Cross-sectional * Calibration from options prices at a single point in time

- Panel * Calibration from options prices at a multiple points in time

Besides, calibration can recover the full parameter set and unobservable state variables or just the unobservable state variables.

The available calibration functions are the following: